Quick overview

Live BTC/USD Chart

BTC/USD

The ECB held interest rates steady while markets absorbed cautious optimism from Lagarde, shifting global data, and quiet volatility across assets ranging from gold to crypto.

ECB Holds Steady, Lagarde Cites Progress and Risks

The European Central Bank left rates unchanged, with President Christine Lagarde offering a cautiously optimistic outlook. She highlighted that the eurozone grew 0.6% in Q1, outpacing expectations thanks to stronger investment, household consumption, and a firm labor market.

Lagarde noted that inflation is aligning closer to the ECB’s 2% target, as rising productivity and moderate wage growth help cool price pressures. Still, she pointed to headwinds such as tariff uncertainty, a stronger euro, and geopolitical instability as potential downside risks.

The ECB reiterated its data-dependent stance, with Lagarde emphasizing that no precommitment is being made regarding the next rate move. The current policy was unanimously supported by the governing council. According to internal sources, September’s meeting is likely to yield no change either.

Across European markets, indices were mixed. France and Italy slipped, while Spain and the UK outperformed.

Central Bank Optics and US Data Stir Markets

Back in the U.S., attention turned briefly to Federal Reserve Chair Jerome Powell, who appeared alongside President Donald Trump during a media tour of the Fed’s remodeled facilities. Trump downplayed any friction, stating there was “no tension” in their conversation about interest rates. However, Powell seemed less comfortable, with markets reading the moment more as political theater than substance.

Economic data offered mixed signals. U.S. manufacturing PMI showed contraction, but the services PMI continued to expand, keeping sentiment afloat in tech-driven sectors.

Wall Street Ends Mixed; Dow Pulls Back

The Dow Jones Industrial Average fell sharply by 316.38 points (-0.70%), retreating from its near-record close on Monday. The S&P 500 barely eked out a gain (+0.07%), setting a fresh record close. The NASDAQ rose 0.18%, also notching a new high—showing ongoing strength in growth and AI-related names.

Today’s Market Events

Tokyo Inflation Eases Slightly in July, Signals Modest Cooling Ahead

Tokyo’s consumer inflation data for July, a closely watched indicator that typically leads Japan’s national figures by about three weeks, showed a slight cooling in price pressures.

The headline Consumer Price Index (CPI) rose 2.9% year-over-year, just below the expected 3.0% and down from 3.1% in the previous month. The core CPI, which excludes volatile fresh food prices, also came in at 2.9%, matching the headline figure and undershooting expectations by a tenth of a percentage point. This, too, marked a decline from 3.1% in June.

The core-core CPI, which strips out both fresh food and energy costs—considered Japan’s closest equivalent to the U.S. measure of core inflation—remained steady at 3.1%, aligning with forecasts and unchanged from the prior month.

While the overall figures point to persistent inflation above the Bank of Japan’s 2% target, the slight easing may offer policymakers some reassurance that price growth is stabilizing. Markets will now look to see whether this early signal translates into a similar trend at the national level later this month.

UK Retail Sales to Rebound in June

In retail data, U.K. month-over-month retail sales are expected to rise by 1.1% in June, reversing the sharp 2.7% drop seen in May. Core M/M sales are forecast at 1.0%. Analysts, including Investec, noted that May’s decline was likely overstated due to prior temporary boosts in volumes.

In the UK, BRC Retail Sales for June rose 2.7% YoY, up from just 0.6% previously. Food sales were especially strong, driven by persistent inflation in essentials.

Last week, markets were slower than what we’ve seen in recent months, with gold retreating and then bouncing to finish the week unchanged. EUR/USD slipped toward 1.16, while S&P and Nasdaq continued higher. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

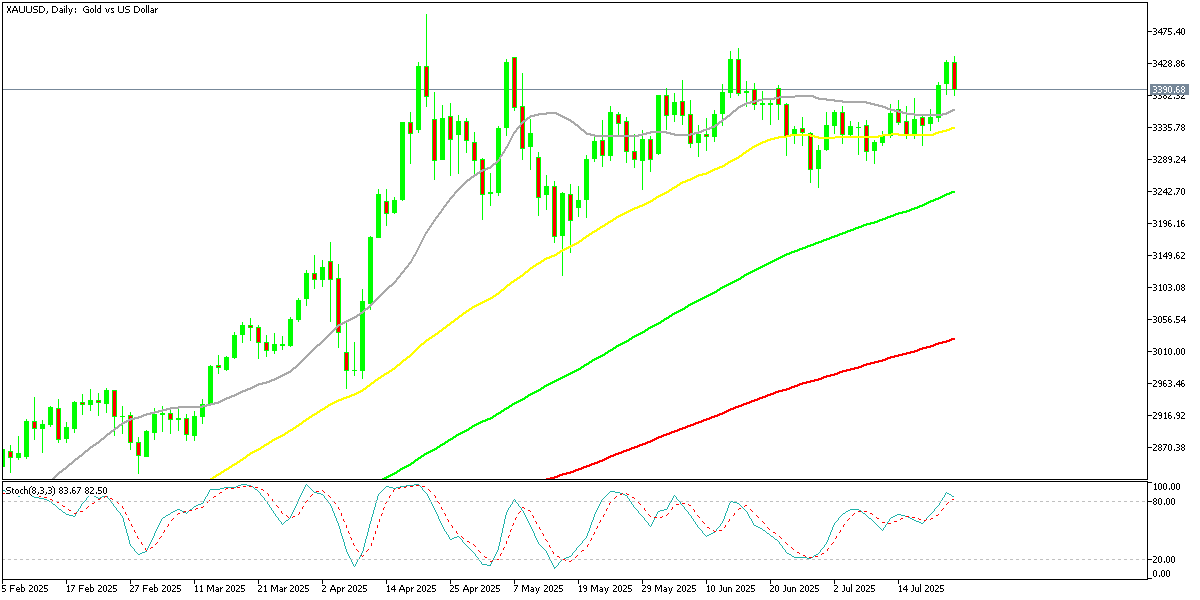

Gold Returns Below $3,400

Gold rebounded off its 20-week moving average near $3,150, climbing nearly $50 to finish around $3,438/oz. Still, after failing to hold above $3,400 post-U.S.-Japan trade talks, gold appears stuck in a consolidation phase below the $3,500 resistance. Traders await fresh inflation clues or remarks from the Fed to trigger the next move.

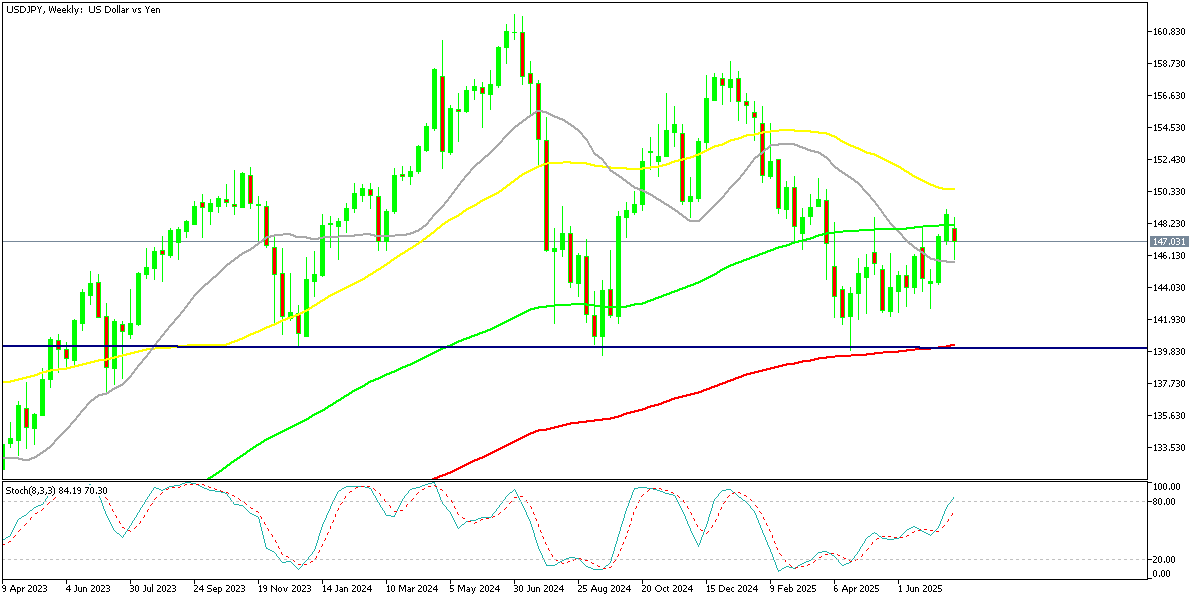

USD/JPY Returns Below the 100 Weekly SMA After Japanese Elections

The USD/JPY pair made headlines as it broke above the 148 handle, a move that defied recent yen strength and pierced the 100-week moving average—often seen as a key long-term resistance marker. This unexpected strength in the dollar is being partly driven by Japanese capital flowing into foreign assets, which is complicating forecasts for future Bank of Japan policy moves. A firm close above this level could shift sentiment and revive debates around policy divergence between the Fed and BOJ.

USD/JPY – Weekly Chart

Cryptocurrency Update

Cryptocurrencies Hold Gains as Bitcoin Briefly Tops $120K

In digital assets, Bitcoin briefly dipped below $113,000 earlier in the week but bounced sharply and reclaimed support above $120,000. The recovery came after testing the 50-day moving average, with strong buyer demand kicking in around the 20-week SMA. Investors appear to be using dips as opportunities to hedge against volatility in traditional markets.

BTC/USD – Weekly chart

Ethereum Breaks Above Resistance, Heads for $4,000

Ethereum has outpaced Bitcoin recently, gaining 20% since April and breaking above its 100-week moving average. Optimism around the upcoming “Pectra” upgrade—which promises scalability improvements—has boosted institutional inflows. With ETH now eyeing the $4,000 level, bullish sentiment in the space is gaining traction.

ETH/USD – Daily Chart

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank’s local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.