Dollar’s broad-based advance continues today, underpinned by firm sentiment that recent US trade deals with the EU and Japan mark the clearing of major global trade risks, at least for now. Though US–China talks continue in Stockholm, markets appear unbothered. Officials on both sides have indicated willingness to negotiate terms and extend the August 12 tariff truce by another 90 days. The absence of escalation risk is helping to sustain a risk-on bias, even if a full breakthrough is still pending.

Euro, meanwhile, continues to lag. Even as EU politicians criticize the terms of the US-EU framework agreement, equity markets seem more constructive. Germany’s DAX and France’s CAC 40 both gained more than 1% in early European trade, lifted by a string of upbeat earnings reports and relief that trade escalation was at least avoided.

This divergence in sentiment is visible across currencies. Dollar tops the leaderboard this week so far, followed by Loonie and Yen. On the other side, Euro is the weakest performer, trailed by the Franc and Kiwi. Aussie and Sterling are stuck in the middle.

Next up, focus turns to Australia’s Q2 CPI due in the Asian session. Headline inflation is expected to slow from 2.4% yoy to 2.2% yoy, continuing the steady down trend from 7.8% yoy peak in Q4 2022. The RBA held rates steady last month on a split vote of 6-3. Since then, jobs data have softened while price growth remains sticky. A soft CPI reading would help cement the case for another rate cut in August.

Technically, AUD/USD has been clearly losing upward momentum since May, as seen in D MACD. But there is not clear sign of topping yet. However, firm break of 0.6453 support will argue that it will at least be correcting the rebound from 0.5913, and target 38.2% retracement of 0.5913 to 0.6624 at 0.6352.

In Europe, at the time of writing, FTSE is up 0.54%. DAX is up 1.10%. CAC is up 1.20%. UK 10-year yield is down -0.017 at 4.638. Germany 10-year yield is up 0.002 at 2.695. Earlier in Asia, Nikkei fell -0.79%. Hong Kong HSI fell -0.15%. Singapore Strait Times rose 0.33%. Singapore Strait Times fell -0.28%. Japan 10-year JGB yield rose 0.006 to 1.575.

ECB survey shows inflation fears recede, growth pessimism softens

Eurozone consumers are dialing back their inflation expectations, according to the ECB’s latest Consumer Expectations Survey for June. Median one-year inflation expectations fell from 2.8% to 2.6%, fully reversing the uptick seen in March and April. Longer-term expectations remained anchored, with three-year and five-year outlooks steady at 2.4% and 2.1% respectively, the latter unchanged for seven consecutive months.

Household sentiment on spending also weakened. Expected nominal spending growth dropped to 3.2% in June, down from 3.5% in May and 3.7% in April. The continued decline suggests rising caution among consumers, likely driven by lingering geopolitical uncertainty, uneven wage growth, and lower perceived price pressures ahead.

On growth, expectations became slightly less negative. Median expectations for economic growth over the next 12 months improved to -1.0% from -1.1% in May and -1.9% in April. Still, households broadly expect economic contraction, reflecting the Eurozone’s fragile recovery and ongoing concerns around trade, manufacturing, and domestic demand.

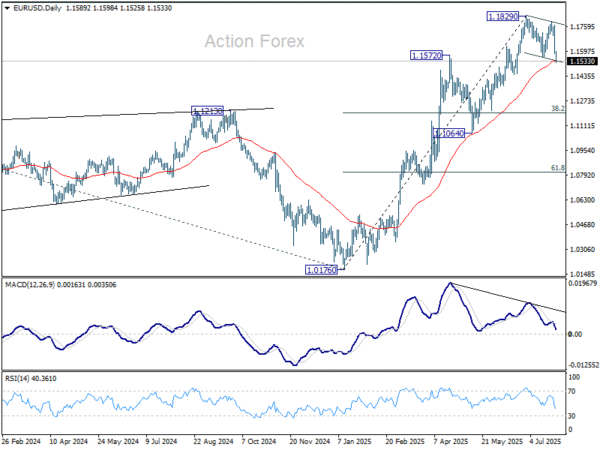

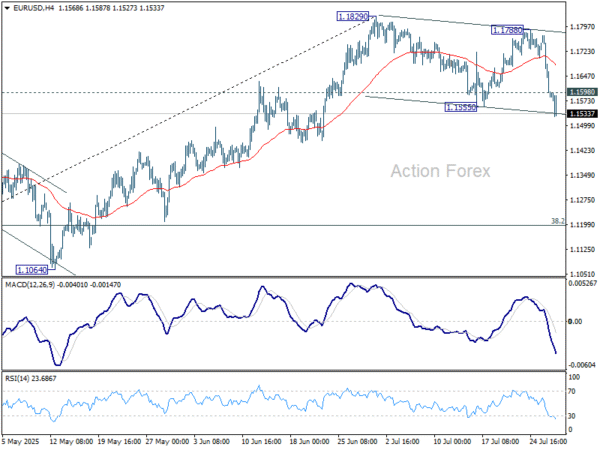

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1526; (P) 1.1648; (R1) 1.1711; More…

Intraday bias in EUR/USD remains on the downside with focus on 55 D EMA (now at 1.1538). Sustained break there will argue that fall from 1.1829 is already correcting the whole rise from 1.0176. Deeper decline should then be seen to 38.2% retracement of 1.0176 to 1.1829 at 1.1198. Nevertheless, strong rebound from the EMA will maintain near term bullishness. Above 1.1598 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.