In the last week, the United States market has been flat, yet it has shown an impressive 11% increase over the past year with earnings projected to grow by 14% annually in the coming years. In this environment, identifying stocks with strong fundamentals and growth potential can be key to uncovering promising opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

NameDebt To EquityRevenue GrowthEarnings GrowthHealth RatingWest Bancorporation169.96%-1.41%-8.52%★★★★★★Morris State Bancshares9.62%4.26%5.10%★★★★★★Metalpha Technology HoldingNA81.88%-4.97%★★★★★★FineMark Holdings122.25%2.34%-26.34%★★★★★★FRMO0.09%44.64%49.91%★★★★★☆Gulf Island Fabrication19.65%-2.17%42.26%★★★★★☆Pure Cycle5.11%1.07%-4.05%★★★★★☆First IC38.58%9.04%14.76%★★★★☆☆Reitar Logtech Holdings31.39%231.46%41.38%★★★★☆☆Vantage6.72%-16.62%-15.47%★★★★☆☆

Click here to see the full list of 284 stocks from our US Undiscovered Gems With Strong Fundamentals screener.

We’ll examine a selection from our screener results.

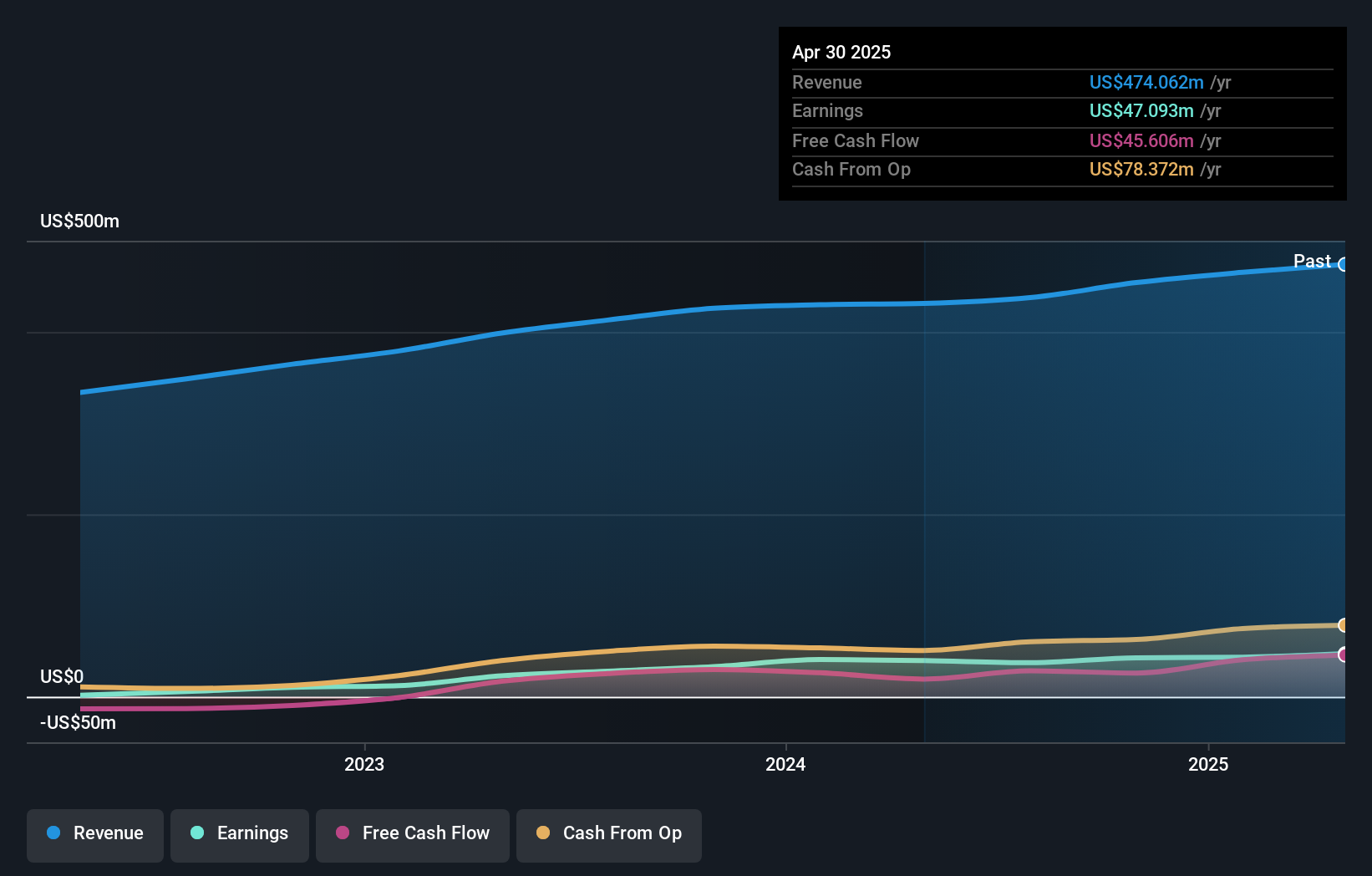

Simply Wall St Value Rating: ★★★★★☆

Overview: China Yuchai International Limited, with a market cap of $643.81 million, operates through its subsidiaries to manufacture, assemble, and sell diesel and natural gas engines for various applications including trucks, buses, construction equipment, and marine use in China and internationally.

Operations: The primary revenue stream for China Yuchai International Limited comes from its subsidiary, Yuchai, contributing CN¥19.10 billion. A smaller segment, HL Global Enterprises Limited (HLGE), adds CN¥30.78 million to the revenue.

China Yuchai International, known for its robust performance in engine sales across various sectors, has shown earnings growth of 13.1% over the past year, outpacing the Machinery industry’s 3%. The company enjoys a favorable price-to-earnings ratio of 15.6x compared to the US market’s 17.8x, indicating good value relative to peers. With a debt-to-equity ratio increase from 17.8% to 20.4% over five years, it still maintains more cash than total debt, ensuring financial flexibility. Strategic partnerships and investments in R&D are likely to support future growth despite challenges like regulatory uncertainties and competition in key markets.

Simply Wall St Value Rating: ★★★★★☆

Overview: Oil-Dri Corporation of America, along with its subsidiaries, specializes in the development, manufacturing, and marketing of sorbent products both domestically and internationally, with a market capitalization of $724.25 million.

Operations: ODC generates revenue primarily from two segments: Business to Business Products, contributing $166.91 million, and Retail and Wholesale Products, contributing $298.43 million.

Oil-Dri Corporation of America, a compact player in the household products sector, has shown robust earnings growth of 6.5% over the past year, outpacing its industry peers. With a net debt to equity ratio at 7.7%, its financial structure appears satisfactory, and interest payments are well-covered by EBIT at 34.8 times coverage. Recent earnings reports highlight an impressive jump in quarterly sales to US$115 million from US$107 million last year, alongside a net income rise to US$11.64 million from US$7.78 million previously. Despite significant insider selling recently, it trades at nearly 77% below estimated fair value, suggesting potential undervaluation for investors willing to take on some risk with this niche company focused on innovative cat litter products and sustainability initiatives under CEO Daniel S. Jaffee’s leadership.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Stewart Information Services Corporation operates through its subsidiaries to offer title insurance and real estate transaction services both in the United States and internationally, with a market capitalization of approximately $1.68 billion.

Operations: Stewart Information Services generates revenue primarily from its Title segment, including mortgage services, which accounts for $2.18 billion, and Real Estate Solutions contributing $372.74 million. The company experienced a net profit margin trend worth noting over recent periods.

Stewart Information Services, a player in the title insurance sector, has seen its earnings grow by 75% over the past year, significantly outpacing the industry average of 5.3%. The company’s debt to equity ratio increased from 13.9% to 31.7% over five years but remains satisfactory with net debt at 18.6%. Recent strategic moves include targeting acquisitions in key Metropolitan Statistical Areas and expanding agency services, which are expected to boost net margins from 2.9% to 6.3%. With a current price of US$65.2 per share and a target of US$78.5, there’s potential for growth amidst market challenges.

Key Takeaways

Curious About Other Options?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com